APR without backtesting in a pool is a scam — and how to avoid it

TL;DR: Most DeFi platforms calculate APR by extrapolating the last 24 hours of fees into a full year, using a formula that ignores the key variables of concentrated liquidity. It's an oversimplistic method, industry-standard, and it basically has you investing blind. In this article we explain why it fails, what backtesting is, and how to use it to make real decisions.

Why that 320% APR doesn't mean as much as it looks?

You've probably landed on a page and found pools showing incredible APRs: 250%! 320%! 60% on stablecoins!

And naturally, you look at those numbers and think: "if Uniswap or Krystal shows it, it must be true". Well, I have some bad news: those APRs are miscalculated or, at best, very unrepresentative of what you'll actually earn. And the worst part is that this isn't a bug — it's the industry standard.

The formula almost everyone uses — and why it fails on two levels

The vast majority of platforms —Uniswap, PancakeSwap, Orca, Krystal...— calculate APR with this formula:

APR = (fees 24h / TVL) × 365 × 100

At first glance it seems reasonable: it uses real data and relates fees to TVL. The problem is that it fails on two distinct levels, and either one alone is enough to take the resulting number with a healthy dose of skepticism.

Problem 1: the base formula is too simplistic

Even before talking about the time projection, the formula has a fundamental mathematical problem: it ignores the variables that actually determine your returns as an LP.

In Uniswap V3 (and any concentrated liquidity protocol), what you earn depends on:

- Your liquidity range: You only earn fees when the price is within your range. Outside of it, you earn nothing.

- Active liquidity in that range: You are not the only LP. Fees are distributed proportionally based on the distribution of liquidity at the time of the swap.

- TVL: Pools with low TVL generate fewer fees.

- Volume: which is used to calculate the fees generated.

- Fee tier: which is used to calculate the fees generated by each swap.

The formula (fees 24h / TVL) × 365 doesn't account for any of this. It divides total fees by

total TVL as if all liquidity were equivalent and always active. In V2 that was approximately

correct. In V3, it falls quite short.

Problem 2: extrapolating 24 hours into a full year

On top of the previous problem, the formula takes a single day of data and multiplies it by 365. If yesterday was an exceptionally high-volume day —a market event, a pump, whatever— that number becomes your "expected annual return". And everyone acts like that's totally fine.

| Day | Fees generated | Projected APR |

|---|---|---|

| Monday (normal day) | $200 | 27% |

| Tuesday (high volume) | $1,400 | 189% |

| Wednesday (normal day) | $210 | 28% |

The same pool, the same week, with a 7x difference depending on which day you look. That's not an acceptable margin of error — it's quite a lot of noise to base an investment decision on.

Putting both problems together: you have a formula that was already imprecise to begin with, applied to a single day of data and presented as your expected annual return. The result is a number that can deviate significantly from reality, and that also swings wildly from one day to the next.

The solution: real backtesting

To avoid investing blind, there's backtesting: simulating how a pool has generated fees over a real period of time, using all the relevant data.

To do it properly, you need to account for:

- Fee tier of the pool

- Liquidity range configured

- Liquidity distribution within that range

- Historical TVL

- Market volume over the analyzed period

With all those inputs you can simulate the real returns of, say, the last 30 days — and get an honest, calibrated estimate, not a 24-hour extrapolation multiplied by 365.

Can we predict the future? No. But if we can't even model the past properly, what basis are we making decisions on? The answer is: very little.

How to verify real returns before entering

The most direct way is to look for tools that offer real backtesting instead of projected APR. Before putting capital into any pool, ask yourself these questions:

- Is the APR I'm seeing based on 24h data or historical data?

- Can I see the performance over the last 7, 14, or 30 days?

- Does the tool account for my specific liquidity range?

If the answer to any of these is "I don't know" or "no", you're operating with incomplete information.

Tools that actually offer real backtesting

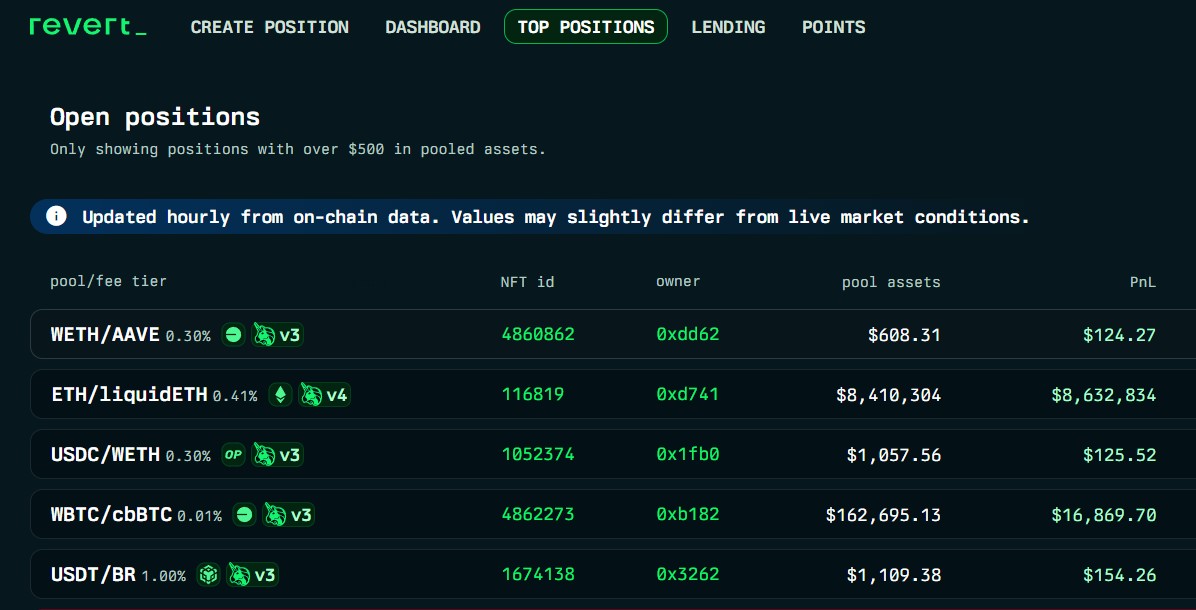

Revert.finance

One of the most established tools in the concentrated liquidity ecosystem. It offers historical position analysis and reliable on-chain data. Very useful for reviewing the performance of existing positions, though its focus is more oriented toward tracking open positions than exploring and comparing pools before entering.

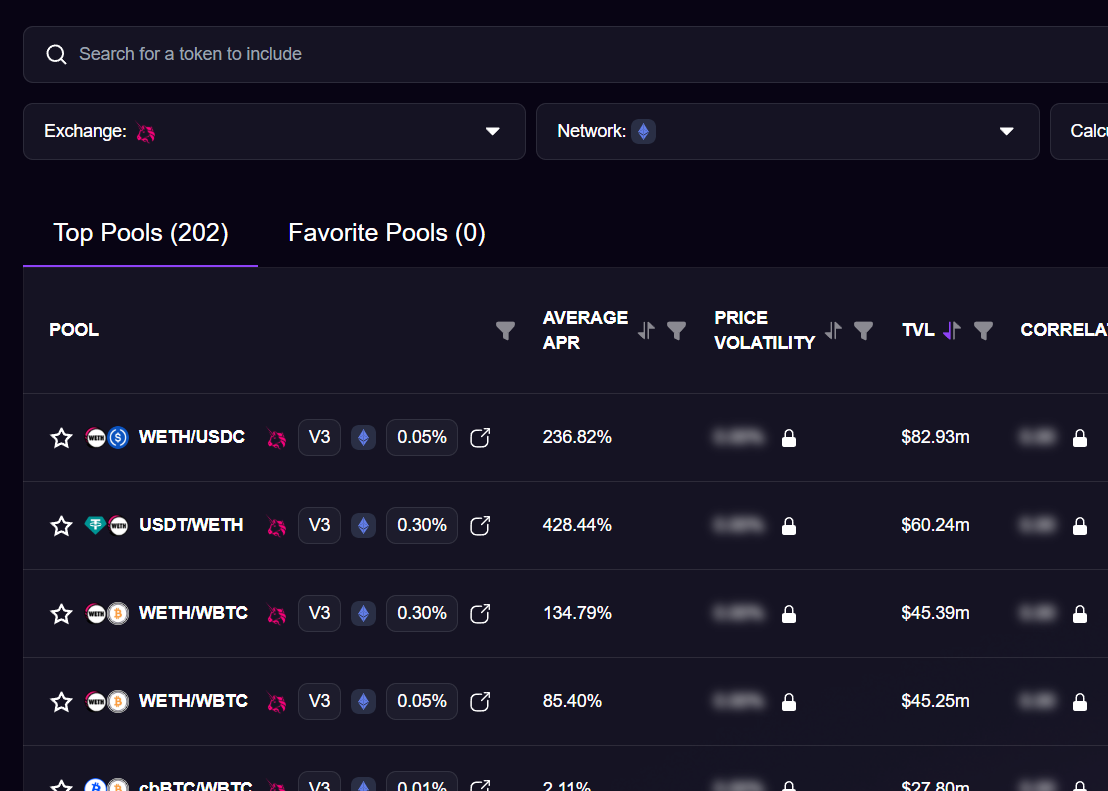

Metrix.finance

A solid reference among more serious LP managers. Its data is reliable and its backtesting is robust. The main drawback is the learning curve: the interface isn't the most intuitive, it can slow down during high-demand periods, and the pro version costs $50/month — a meaningful barrier for retail users.

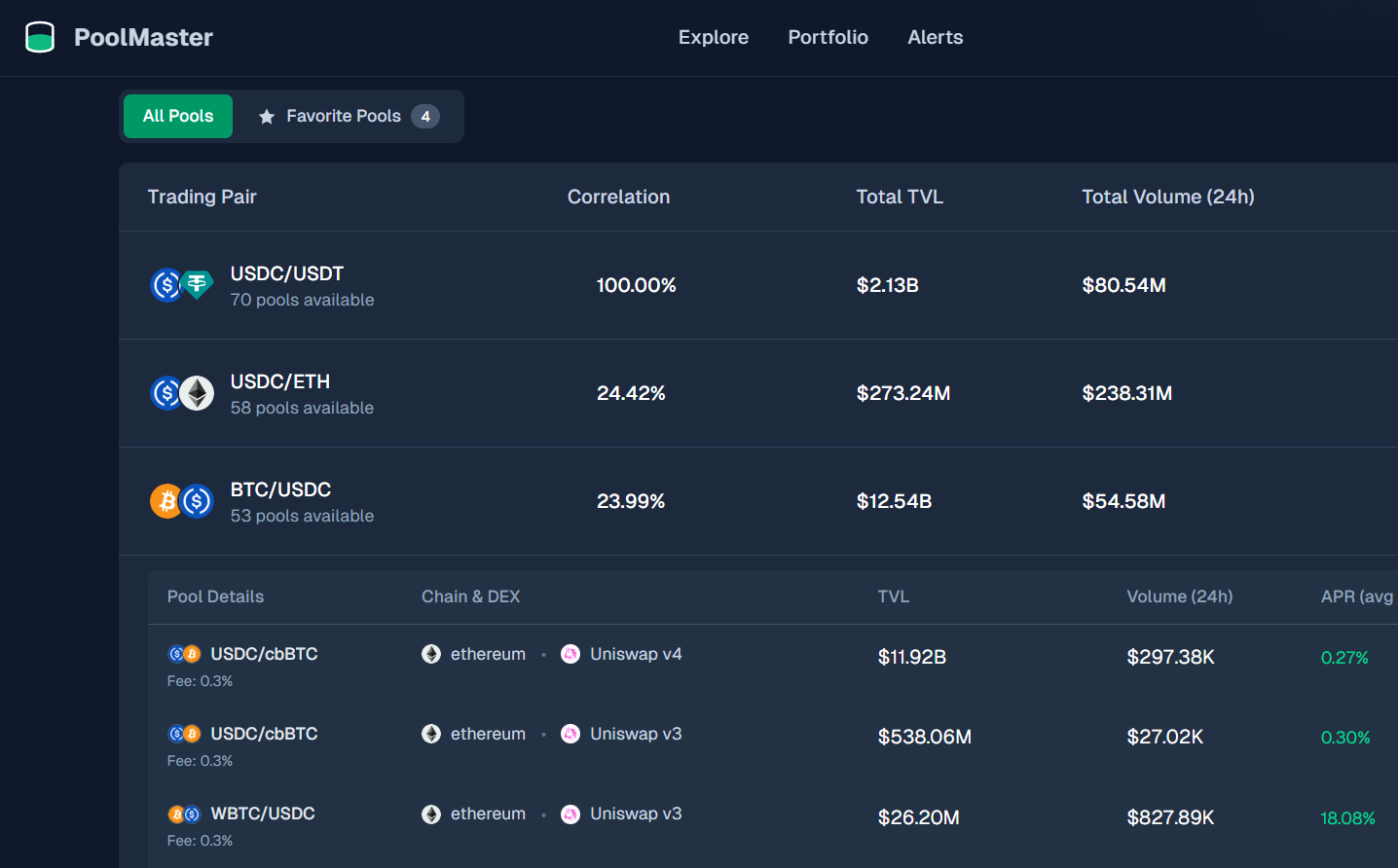

Poolmaster.io

The most recent alternative and, probably, the most accessible for most users. In addition to offering real backtesting, its key differentiator is that it groups pools by token pair: you can see that same pair across different platforms (Uniswap, PancakeSwap, etc.) in a single view and compare which one has historically performed better — something that, surprisingly, no other tool had done clearly before.

Instead of searching pool by pool, you find directly the best pool for that pair. Backtesting included.

The tool is 100% free on its base version, with a PRO plan for advanced users.

💡 Exclusive discount: If you want to try Poolmaster PRO, use the coupon

POOLMASTER_STARTERto get a 25% discount.

Conclusion

Projected APR from 24-hour data is, at best, a simplification that's worth understanding before using it to make decisions. At worst, it's the reason many LPs exit a pool wondering where the returns they were expecting went.

Backtesting doesn't eliminate risk — no tool does. But it gives you a much more solid foundation to decide. The difference between projecting one day and analyzing 30 is the difference between intuition and judgment.

If you found this article useful, share it — there are a lot of people choosing pools based on data that doesn't tell the whole story.